Global cryptocurrency adoption remains on course to reach approximately 750 million users by the end of 2023, according to Triple-A.

Per the report, the top five countries by the estimated number of holders are the U.S., India, Pakistan, Nigeria, and Vietnam at 46 million, 27 million, 26 million, 22 million, and 20 million, respectively. Vietnam’s ownership percentage came in at 26% of the population, with the U.S.’s at 13.2%.

The U.K. placed low, having just 3.7 million estimated holders, representing 5.5% of the population. But despite falling short on cryptocurrency adoption metrics compared to other countries, the U.K.’s ruling Conservative party has signaled its intent to incorporate digital assets into its economic plans.

In January, despite the fallout from the FTX collapse continuing to linger, Economic Secretary to the Treasury Andrew Griffith spoke about championing cryptocurrency and blockchain technology to bring about future economic benefits.

Griffith said he fully intends to turn the U.K. into an advanced financial center, which “absolutely [has] room” for cryptocurrency and blockchain technology.

The wording used by Griffith suggested cryptocurrency will play second fiddle to the pound. But reading between the lines, might Griffith be intentionally downplaying the importance of digital assets to the U.K.? Especially considering the pound’s decline.

The British pound

Historians noted that during Anglo-Saxon times, from 410-1066AD, one pound was the equivalent of a pound weight (454 grams) of silver, a considerable fortune at the time.

However, it wasn’t until 1815–1920 and the rise of the British East India Company, a trading body for English merchants, that the pound rose among global currencies rankings to assume the role of reserve currency.

Although the pound lost its reserve currency status to the dollar under the Bretton Woods agreement, it wasn’t until the 1970s, as U.S. President Nixon “suspended” the dollar’s convertibility to gold, that the pound’s decline became undeniably apparent.

In 1976, faced with a financial crisis, the U.K. government was forced to seek a $4 billion IMF loan. Contributory factors to the situation included a spiraling balance of payments deficit, excessive public spending, and the quadrupling of oil prices.

Adjusted for inflation, $4 billion in 1976 equals $21.03 billion in today’s money – a cumulative increase of 426% over 47 years.

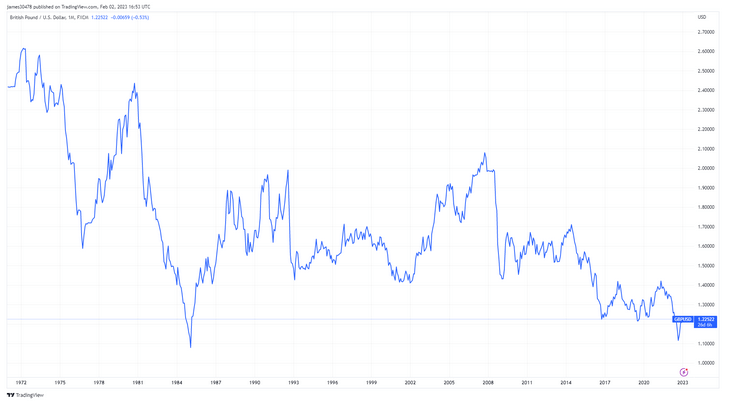

The chart below shows a dollar was valued at around £2.60 in 1972. By the mid-80s, this had plummeted to as low as £1.10, spurred in part by a general decline in British industry, including the end of the coal mining sector, and dollar strength resulting from significant tax cuts by President Regan.

Dwindling global influence

The late 80s saw a reversal of downward pressure on the pound as the country went about redefining itself as a service economy – particularly in respect of financial services. But the macro downtrend re-exerted itself following the start of the last recession in 2006.

Further down pressure came in 2016, as the U.K. left the E.U. under the Brexit referendum and, more recently, via the economic naivety of former Prime Minister Liz Truss, who triggered market panic due to her “mini-budget” of unfunded tax cuts, causing the pound to crash to near 1985 lows.

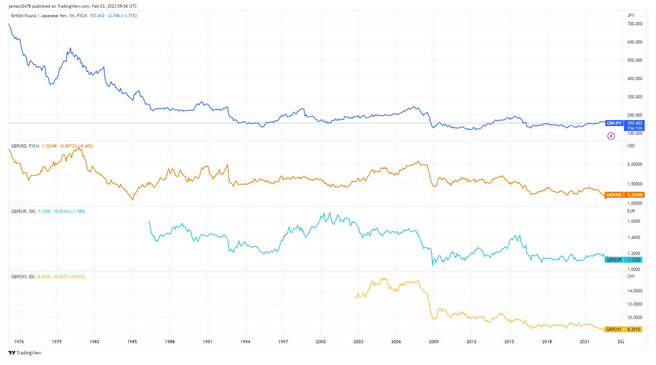

Far from being an isolated trend against the dollar, since the 70s, the pound’s value against other major currencies, such as the yen, euro, and yuan, has also collapsed. For example, in 1976, one pound could buy 700 yen. Today, the rate is closer to 150 yen – a near 80% decline in value.

The pound’s decline runs in lockstep with the U.K.’s dwindling influence on the global stage. Calling Britain and the pound a shadow of their former selves would be a polite way to frame the situation – something Westminister is fully aware of.

Why is the U.K. looking to digital assets?

In recent times, the U.K. government has signaled its intent to regulate cryptocurrencies, thus sanctioning their legitimacy within its jurisdiction.

A post from the Treasury dated Feb. 1 highlighted proposals to regulate financial intermediaries, including crypto exchanges, laying the groundwork for a friendly regulatory landscape.

“These steps will help to deliver a robust world-first regime strengthening rules around the lending of cryptoassets, whilst enhancing consumer protection and the operational resilience of firms.”

But to what degree are these actions directed by a sincere belief in cryptocurrency tenets? After all, Bitcoin is the antithesis of centralization and is ideologically incompatible with control structures outside of personal sovereignty.

The Treasury is probably willing to cede a proportion of its monetary monopoly in exchange for the potential economic benefits of national cryptocurrency adoption. This call is likely driven by an understanding that cryptocurrency adoption will increase over time.

As such, far from advocating cryptocurrency tenets, it’s more likely the U.K. is positioning itself favorably in readiness for mass adoption.

People are not happy with the financial system

While legacy system cracks began showing as far back as 1976, the last year saw an acceleration of the pound’s decline as funny money policies in response to the health crisis took effect.

U.K. households are experiencing a significant fall in disposable incomes, and everyday people are struggling amid the cost of living crisis – making it increasingly evident that the system is broken, even to lay people who may not be fiscally informed.

In the past, Brits bought property to counter inflation and currency debasement. But with house prices being 11 times the average salary for Londoners, affordability is currently running well past sustainable levels.

The lack of (traditional) options to park money amid an environment of dwindling purchasing power has fostered more dissatisfaction with the financial system. Under such circumstances, people will seek novel alternatives, including cryptocurrencies. For that reason, the worse things get, the more cryptocurrency adoption will advance.

It’s very telling that developing countries, where financial inclusion and economic stability are typically low, thus sowing economic dissatisfaction, make up four out of the five top spots for the estimated number of cryptocurrency holders.

In rubber stamping cryptocurrencies, the U.K. Treasury has inadvertently admitted that people are losing faith in the pound and legacy economic system.

But in fairness, diminishing confidence in the local currency is a problem facing all countries, not just the U.K. As the global legacy system continues floundering, expect cryptocurrency adoption trends to accelerate.

CBDCs – the elephant in the room

The Deputy Governor of the Bank of England (BoE,) Sir Jon Cunliffe, told the Treasury Select Committee that the U.K. is 70% likely to launch a digital pound Central Bank Digital Currency (CBDC).

Critics argue that CBDCs present risks to privacy and could be used for financial manipulation by governments and central banks, particularly regarding restricting transactions and taking away people’s right to transact freely.

The commitment to both private cryptocurrencies and a digital pound raises questions about the U.K. government’s vision of an advanced financial center – as the two are philosophically incompatible.

It remains to be seen how the Treasury will mesh its crypto hub vision with the digital pound, should it see the light of day.